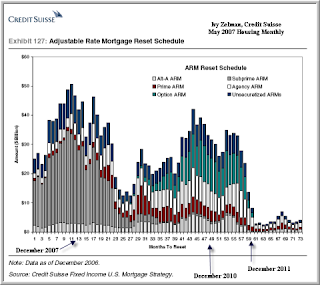

The above is a very familiar chart showing ARM re-sets. ARMs are problematic for several reasons:

For Lenders: these represent the bulk of outstanding loans.

For Borrowers: Many are finding themselves in a hole due to stricter lending and higher mortgage rates. Gone are the 4% teaser rates - ARMs are at least 100 basis points higher than they were a few years ago. And even if they could jump the hurdles of tighter credit standards, many would not get the full loan re-financed. Unfortunately, property losses are severe and many lenders demand downpayments

Let's ignore the lenders: we're more concerned about the consumer side of the equation.

How thin is the ice?

According to the Federal reserve, California owner occupied homes:

72% of all loans are variable

Mortgage rates and home prices are central to the California housing market. With home prices now at 2003/2004 levels, that means that the homes re-setting are also under water: the value of the home is less than the loan.

So how are folks doing?

% of loans not current: 42%

% 2 months delinquent: 9.3%

% 3 months delinquent: 5.6%

% >3 months delinquent: 8.2%

The rest are REO or in foreclosure

And a whopping 25% loans have no documentation - aka liar loans.

Not only are folks facing problems re-financing their homes. California is leading the nation for withdrawing 'equity' from the home: only 38% of all loans went to home purchases. Fully 45% of all loans were for cashing out.

A lot of belt tightening is about to hit California. Some 43% of all California ARMs are due to re-set in the next 12 months.

It's a death spiral in action as the entire housing boom unwinds.

Look at the Bay Area. The Median home price requires a Jumbo loan. The rates for Jumbo ARMs are almost 6%. In addition, to qualify, most have to now have downpayments.

By the end of this Summer, the Subprime ARM wave wil have subsided. But the next wave will be just starting: Prime and Alt-A. In theory, these folks can re-finance easier (they have better credit histories). But in reality, they will face the same big hurdle: lenders will not loan more than the house is worth. And the house in late 2008 will be worth a lot less than the original loan amount.

And many of these supposedly solid credit borrowers used 2 mortgages to afford the home.

It's possible that mortgage rates will fall by then, but not enough to offset the drop in property values. This will be the reality throughout 2009 and 2010.

You can expect a lot more inventory this time next year. By 2010, nobody will be looking to buy a home, which is exactly when one should buy a home.

Late 2008 is when things will pick up steam:

* Mainstream media will be reporting that housing is in a long term bust and prices will drop - this will reduce demand and, at the same time, motivate sellers to price competitively

* Recession will be biting hard, further reducing demand

* Banks will have surging inventory of repossessed homes

* Weak 2008 summer sales will push banks to unload their inventory at fire-sale prices

By 2009, inventories of distressed housing will surge again. This will scare both buyers, sellers, and lenders. By late 2009, housing will be like a ghost town. Then another surge in 2010 will seal the deal: housing will be the last place folks will buy.

Further affecting things will be the drop in municpal and state taxes. Homeowners will force tax re-assessments. The consequent plunge in services will drive an outflow of residents. Folks will simply move to other, cheaper states.

Then add corporate pressure. Many companies will be tempted to move out of state to preserve margins. To be honest, a great way to cut the payroll is to simply move the team to Colorado or Arizona. This is more insidious because it is the long-term lifeline of the State's income.

California property is about to be as famous as Florida swampland. It will take years to recover.

Shift gears away from housing and focus on consumer spending. If Californians are struggling to pay off loans, they won't be partying in Vegas or dancing all night in LA clubs. The Californian economy is going to sag. Which may be a good thing for the infrastructure: fewer kids in school, fewer cars on the road, etc. But local economies are going to get desperate.

And California is a major driver of the US economy.

This is why I am short the consumer spending stocks, among others.

If I am reading the data correctly, we could see a 15 point rally from the recent bottom. Possibly as high as 14,000. But then it will collapse to 11,200 really fast.

If I am reading the data correctly, we could see a 15 point rally from the recent bottom. Possibly as high as 14,000. But then it will collapse to 11,200 really fast.

{kind=link}