This week's pullback is just a test

After some lofty gains, the market has pulled back sharply the past 2 days. I actually see this as a normal pull back after a large run up. The DOW surged 3% since August 1st and the NASDAQ 4%. Also, note the resistance today - the NASDAQ has climbed back to almost even.

Part of the problem is that there is very little real news and data until Friday the 15th. Meanwhile, the conflicting signals from the cooling economy and the tight jobs market is making the market jittery. It's all about the Fed. Will he or won't he.

I could spin any number of scenarios that would justify a rate hike or continued pauses. I certainly don't see a rate reduction in the face of job inflationary pressures and continued consumer spending.

I will point out that low unemployment and wage pressures are classic signs of the last phase of a business cycle. And wage pressure matters because salaries are the biggest inflationary contributor. Oil prices have surged 50% in the past year, but the impact on prices has been neglible. CPI is running at less than 3%.

So we can stack on one side a list of inflationary signs (wage pressure, higher than desired CPI, tight job market) and we can stack on another side deflationary signs (falling steel prices, softening oil prices, negative CPI last month, falling housing prices). I think that the Fed knows the housing market will drag the economy down and that will temper inflationary pressures more than a 0.25% increase in interest rates.

Meanwhile, I like the resistance I've seen the past five days in certain stocks:

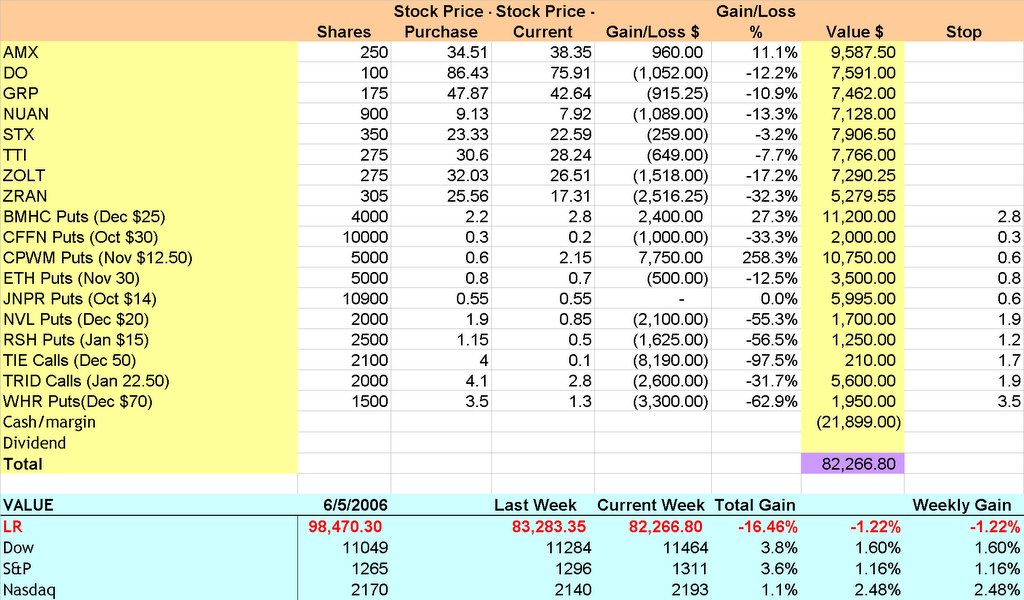

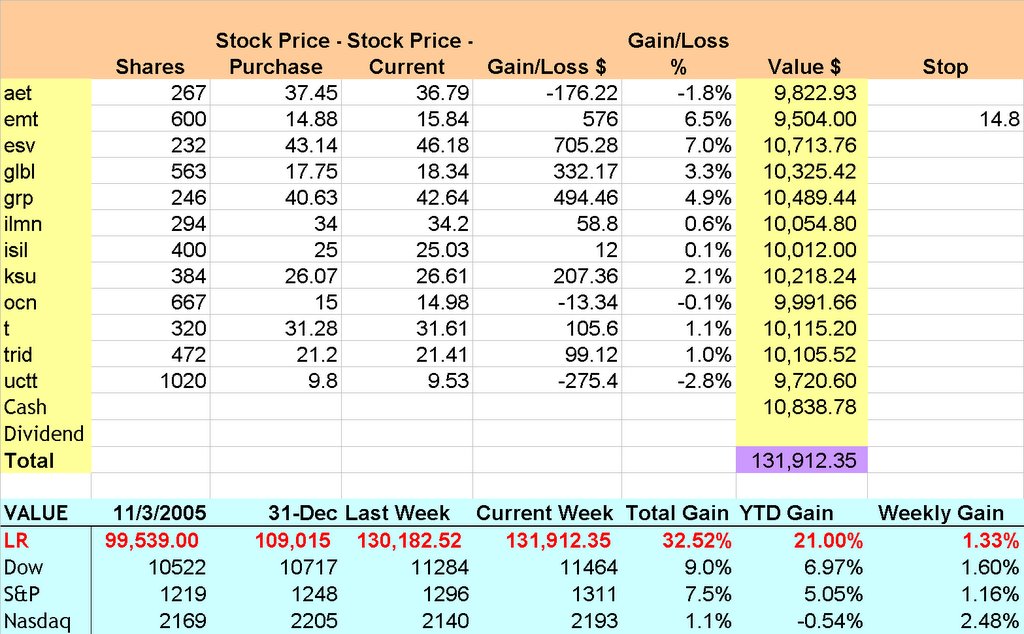

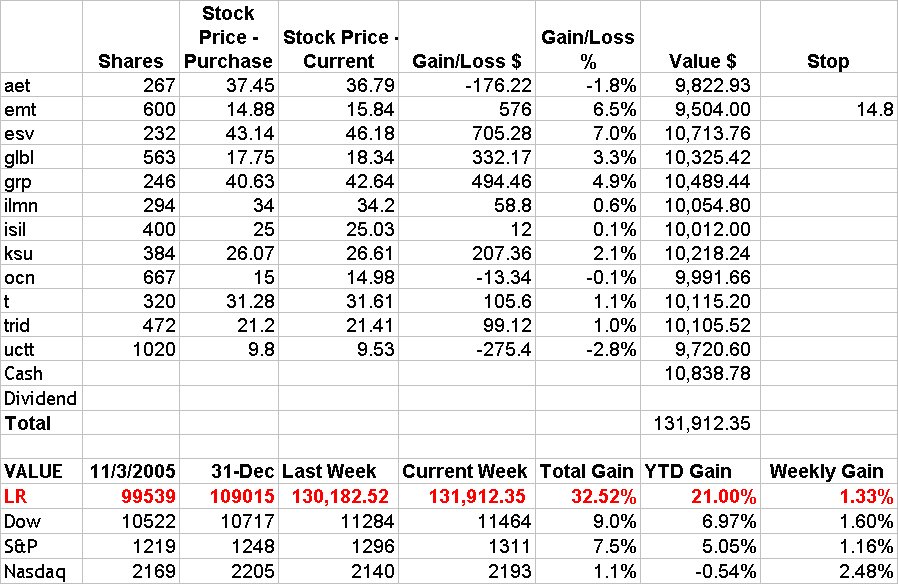

DO - Still up 5% (and up today all day)

ESV - Up 5%

GRP - Up 2.5%

GLBL - Up 1% (and up another 1.5% today)

ILMN - Flat

JLG - Up 6%

KSU - Up 1.5% and up 0.5% today

OCN - Flat

ZOLT - Up 5% (and up 2.3% today)

TTI - Up 4%

And so on. Notice that the oil equipment companies are doing very well.

Part of the problem is that there is very little real news and data until Friday the 15th. Meanwhile, the conflicting signals from the cooling economy and the tight jobs market is making the market jittery. It's all about the Fed. Will he or won't he.

I could spin any number of scenarios that would justify a rate hike or continued pauses. I certainly don't see a rate reduction in the face of job inflationary pressures and continued consumer spending.

I will point out that low unemployment and wage pressures are classic signs of the last phase of a business cycle. And wage pressure matters because salaries are the biggest inflationary contributor. Oil prices have surged 50% in the past year, but the impact on prices has been neglible. CPI is running at less than 3%.

So we can stack on one side a list of inflationary signs (wage pressure, higher than desired CPI, tight job market) and we can stack on another side deflationary signs (falling steel prices, softening oil prices, negative CPI last month, falling housing prices). I think that the Fed knows the housing market will drag the economy down and that will temper inflationary pressures more than a 0.25% increase in interest rates.

Meanwhile, I like the resistance I've seen the past five days in certain stocks:

DO - Still up 5% (and up today all day)

ESV - Up 5%

GRP - Up 2.5%

GLBL - Up 1% (and up another 1.5% today)

ILMN - Flat

JLG - Up 6%

KSU - Up 1.5% and up 0.5% today

OCN - Flat

ZOLT - Up 5% (and up 2.3% today)

TTI - Up 4%

And so on. Notice that the oil equipment companies are doing very well.

posted by Andrew at

9:05 AM

1 Comments

![]()

{kind=link}